Wait! Before you start reading my article about MRTA & MLTA.

Should you even care about MRTA or MLTA ? Is MRTA or MLTA important to you ?

NO, MRTA or MLTA is not important if you’re buying property in cash. Therefore, you can completely skip my article. However, if you’re purchasing property by bank loan / mortgage then I strongly advise you to finish my article because I’ve summarized them here after referring and researching those articles on Google too plus my personal knowledge and comment.

Before we start let’s get started with the full name of the terms:

MRTA: Mortgage Reducing Term Assurance

MLTA: Mortgage Level Term Assurance

MRTT: Mortgage Reduction Term Takaful

MLTT: Mortgage Level Term Takaful

Don’t be scared by those technical terms like ‘MRTA’, ‘MLTA’, ‘MRTT’, and ‘MLTT’ & etc. They are all INSURANCE. Like the other functions or ultimate aims of insurance – PROTECTION.

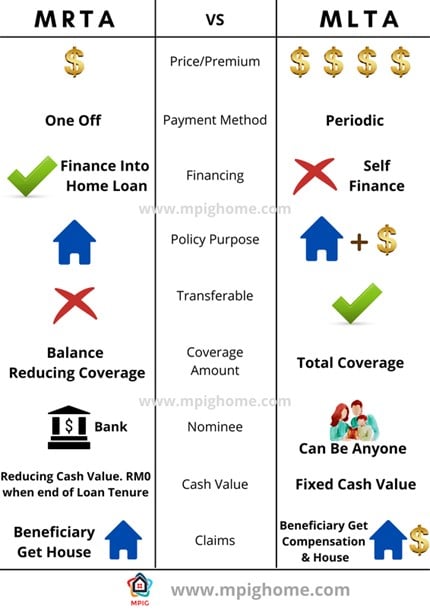

If you don’t like article or you only prefer short and simple answer you can refer the the comparison table I’ve prepared & downloaded from mpighome.com

| MRTA / MRTT | MLTA / MLTT | |

| Cover | Death and Total Permanent Disability | |

| Policy Payments | One-off lump sum payment at start of plan | Can one off, can by monthly instalment |

| Insurance company Pays To | Bank or financial institution holding the home loan | Bank up to the value of outstanding home loan. + Additional funds to beneficiaries |

| Cost | Cheaper than MLTA / MLTT | Expensive than MRTA / MRTT |

Let’s get started now.

Buying your own house / property is one of the major life decisions, being cheated in the process of buying and ended up paying unnecessary money is the last thing you’d ever want.

Unfortunately, there’s still many people out there who are not clear about the process and additional fees and requirements when buying a house or property, even this is not the first time of purchasing. Today we gonna talk about the housing loan / mortgage insurance where most of us often hear the word MRTA, MLTA bla bla bla bla bla so many technical terms.

During / upon approval of your housing loan application, the bank will request you to sign an offer letter. At the same time, your banker/ broker/ insurance agent may tell you that the bank requires you to purchase MRTA or MLTA, which is a form of insurance to protect the interests of both the borrower (you) and the lender (the bank).

This kind of “housing loan insurance” is here to cover the financial burden of your home loan in the event of death and/or total permanent disability.

BE CARERFUL! The insurance company might not pay or settle the whole debt of yours, it all depends on your premium and coverage that you’ve bought.

Well, your next question might be “just tell me which one of them is the best”

I’m sorry, there’s no “the best” but only the most suitable. Just like I’m a property agent (property negotiator) and what looks like the best house/ property for me might not be the best for my client. Just be patient and I promise you my article will not waste your time.

Are these housing loan insurance COMPULSORY by the banks?

NO, NO , NO , a big F**KING NO, sorry for the bad words this is just to get you pay your attention here although you can’t really hear my voice. I really hate hiding and misleading information. Some bankers will tell you the insurance is compulsory but no.

But to be honest, you must buy. Why? Well don’t hate the banks because they want protection too and the mortgage consultants or bankers they need to hit their target / KPI (key performance indicator).

If you buy the insurance, the bank gives you a better / lower interest rate, not that much but yeah we are human beings, we want more benefits. So some banks will ask you to buy a “minimum” insurance premium so that they can offer you a better interest rate.

You can choose to pay the insurance premium in cash or finance into the housing loan, some banks allow you to finance the insurance premium into your housing loan / mortgage for about 5% to 10% of your property purchase price, not possible for me to list them all here because it might change from time to time and it is different from banks to banks.

To be honest sometimes when you buy the housing loan insurance and the banks say to offer you a better rate, after you finance your insurance premium into the loan, your monthly instalment is still the same as if without the so called “better rate” as the one without “better rate”. Mark my word, only sometimes or some cases, not all the time. (you can ignore me if you don’t understand)

Are we really benefit from the house loan insurance as a consumer / purchaser?

Yes, a big yes, just buy it and yes although the bank might earn some extra money from the insurance company but just ignore it. Let it go.

If anything bad happens after purchasing MRTA / MLTA?

You can “rest in piece”

Do these insurance come with Critical Illness (CI)?

Usually no but certain banks will package for you. Remember to clarify.

How much these house loan insurance cost?

My answer? It depends. The cost of the insurance depends on a number of factors such as your age, the value of your home loan, and the length or tenure of your home loan.

The cover or premium is paid with a single lump sum at the beginning of the policy or loan tenure.

The older you are, the riskier you are and therefore the higher the insurance premium you have to pay. Best solution? Buy when you’re young. Also, the higher the value of your home loan, the higher the financial risk.

Oh by the way, sometimes the insurance premium also affected by the nature of your occupation. If you’re smoker, high rise occupation like construction, or KungFu movie actor like Jackie Chan, good news for you, it is either an even HIGHER premium than the others like teachers, accountant & etc or the insurance company won’t even accept you as their client.

Is the housing loan insurance premium refundable?

Yes, I saw some articles said no for MRTA but actually yes it is refundable but ONLY IN ONE CONDITION which is you are able to settle your housing loan earlier than your insurance coverage period and your loan tenure. But, your can only get a very very minor or tiny portion of your MRTA premium, so, forget it.

FAQs About MRTA

The “R” word here is REDUCING and just like the term, home loan insurance where the sum insured is designed to reduce over the term of your home loan.

As you pay off your home loan, the value of your outstanding debt or we call it “principal” will fall or decreasing overtime. Chinese call it 母金.

WARNING! Please insure full amount or even higher than your loan amount also no problem.

Reason? If the amount insured in MRTA is less than your home loan / mortgage at the point of claim = GG.com. If it is not funny just ignore me, trying to be humorous so that the article won’t be too boring, at the point of writing I’m planning on a video explanation too, I will try to insert at the top and bottom and possibly uploading to YouTube and facebook too so if you enjoy my articles help me share it.

Ok come back to our answer. Why it will be a serious problem if your sum insured is less than your mortgage or loan amount? Obviously if you only insured RM 500,000 while you’re taking RM 1million loan, what do you think gonna happen if anything bad takes place? You will have to fork out your own money to cover the difference.

However, if you’re insured for more money than is owed on the home loan, only the amount owed or outstanding loan will be paid out to the home loan provider/ bank, with no additional benefit or extra cash to you like MLTA.

(sample of graph for you to roughly understand the MRTA if you don’t like numbers or graph just skip it, totally ok.)

Here’s a MRTA graph if you like something visual. I got it from https://prestigerealty.com.my/mrta-mlta

Does MRTA come with Critical Illness (CI)?

It depends on your financier or banks package for you or not.

Is MRTA Compulsory?

No, MRTA is not compulsory by the banks. I’ve explained the reason on top, you can find it at the section “Are these housing loan insurance COMPULSORY?”

How Much Does MRTA Cost?

Check with your bankers when you’re applying your housing loan / mortgage, usually they will inform you.

Is MRTA refundable?

Generally speaking, NO. But I’ve explained at the above section “Is the housing loan insurance premium refundable?”

What is MLTA? MLTA Meaning

Mortgage Level Term Assurance (MLTA) is a type of home loan insurance where the sum insured remains level throughout the term of the plan. That means it will pay out the same amount in year 10 as it would in year 25. For example, you insure the amount of RM 1million where your outstanding mortgage is RM 500,000, the insurance company will settle your outstanding debt and you or your beneficiary will receive extra RM 500,000 cash as well, this is the benefit of MLTA where MRTA don’t have.

(tips to differentiate the MLTA & MRTA, the word “R” stand for reducing, so you can just memorize MRTA is the cheaper insurance policy will do. If you prefer to memorize both you can take my suggestion to memorize the word “L” as LIFE. As the word itself shows that LIFE is precious, so it will be expensive and more benefits than MRTA)

(sample of graph for you to roughly understand the MLTA if you don’t like numbers or graph just skip it, totally ok. I got the graph here: https://prestigerealty.com.my/mrta-mlta)

FAQs About MLTA

Is MLTA Compulsory?

Same as MRTA, MLTA is not compulsory. But most of the banks will recommend you take MRTA. Why? Here comes the only bad or disadvantage of MLTA. What? MLTA is bad? Yeah, it is only bad if you have limited budget.

Pro & Con of MLTA?

Better than MRTA but expensive than MRTA. You might not be able to finance whole amount of MLTA into your housing loan / mortgage because there’s limit imposed by the bank like mentioned at the above.

| RM | |

| Loan amount / mortgage | RM 500,000 |

| (depend on bank’s package or TnC) 5% or 10% insurance | RM 25,000 Or RM 50,000 |

Means to say in this case you can only finance your insurance premium about RM 25,000 or RM 50,000 depends on the banks TnC because it might change from time to time.

If you’re younger of course your insurance premium will be lower, so most of the buyer will choose as lower or as minimum insurance premium as possible to lower the monthly loan instalment but if you’re financial capable, just take the MLTA before you regret unless you have made your decision that you will only buy 1 property throughout your whole life. Which in most cases nowadays we are aware of the importance of property where people won’t just aim to buy 1 property.

The exact figure you will have to check with your insurance agent or your banker during the loan application and they will key in your information like age, occupation & etc into their system to generate the premium for you. Don’t worry it’s just a quotation, will not be final or you will be forced to take it.

How much does MLTA cost?

Usually from the cases that I know, MLTA usually cost at least double the MRTA premium, AT LEAST. Remember to check with your banker / insurance agent.

What is MRTT?

You can take it the same as MRTA just that Mortgage Reduction Term Takaful (MRTT) is in ISLAMIC version or known as TAKAFUL. Technically there’s some difference but for the sake of your understanding and to make the article not that “LONG”, so I will just tell you it is the same.

FAQs About MRTT

Is MRTT compulsory?

No, MRTT is not compulsory by the banks. I’ve explained the reason on top, you can find it at the section “Are these housing loan insurance COMPULSORY?”

How much does MRTT cost?

Check with your bankers when you’re applying your housing loan / mortgage, usually they will inform you.

Is MRTT Refundable?

Generally speaking, NO. But I’ve explained at the above section “Is the housing loan insurance premium refundable?”

What Is MLTT?

You can take it the same as MLTA just that Mortgage Level Term Takaful (MRTT) is in ISLAMIC version or known as TAKAFUL. Technically there’s some difference but for the sake of your understanding and to make the article not that “LONG”, so I will just tell you it is the same.

FAQs About MLTT

Is MLTT compulsory?

No, MLTT is not compulsory by the banks. I’ve explained the reason on top, you can find it at the section “Are these housing loan insurance COMPULSORY?”

How much does MLTT cost?

Check with your bankers when you’re applying your housing loan / mortgage, usually they will inform you.

What Are the Differences Between MRTA, MLTA, MRTT, And MLTT?

MRTA vs MRTT ; MRTA vs MLTA ; MLTA vs MLTT

Good news, I’ve summarized them for you here at the table.

| MRTA / MRTT | MLTA / MLTT | |

| Cover | Death and Total Permanent Disability | |

| Policy Payments | One-off lump sum payment at start of plan | Can one off, can by monthly instalment |

| Insurance company Pays To | Bank or financial institution holding the home loan | Bank up to the value of outstanding home loan. + Additional funds to beneficiaries |

| Cost | Cheaper than MLTA / MLTT | Expensive than MRTA / MRTT |

Which Mortgage Life Insurance Is Best For You?

Every individual’s circumstances are unique, which means there’s no clear ‘best mortgage life insurance’ for everyone.

Finding the right cover for you is about assessing the different covers highlighted above, and identifying which policy will best meet the needs of your loved ones in the event that the worst happens.

This cover can be a valuable financial safety net in difficult times, so it’s worth considering even if it’s not a mandatory requirement of your home loan offer.

It’s better to plan for the worst and hope for the best than going the other way around. If you’re not sure which cover is for you, then speak to a financial expert.

Important!

1. Remember to declare your occupation, health condition & etc

because if anything happens the insurance company may claim that you’re not honest and did not disclose the information therefore causing your whole insurance policy to be void!

2. Both the MRTA and MLTA are transferable!

You can transfer your MRTA to the next property that you buy. But again generally speaking by the time you want to transfer your MRTA might not cover that much amount anymore. So it is better I say NO, MRTA no transferable to another property.

For example, you purchase MRTA for Property A, worth RM500,000. You pay a one-time premium of RM11,500 for the MRTA. Five years later, your coverage reduces to RM400,000 (your MRTA coverage reduces over time, hence the term “reducing term”).

Later, you decide to move into a smaller property unit or to purchase extra property – let’s call it Property B and it is valued at RM350,000. If you choose to sell Property A, you have the option of transferring your existing MRTA to Property B, since the remaining MRTA coverage is about RM400,000, and is hence sufficient to cover Property B.

However, if you choose to buy a higher valued Property C, cost RM600,000 – your existing MRTA coverage will not be sufficient to cover for the risks. In this case, you have the option of topping up for the remaining RM200,000 coverage (unless you like to live dangerously).

In some cases, it might make more financial sense to purchase a new policy rather than topping up an existing one. Transferring MRTA from one bank to another is also complicated. Terms and conditions also vary from bank to bank and insurance company too. Check with your local bankers (whom you can trust) to find out which option is best for your situation.

3. You can co-own the mortgage insurance

if you have jointly purchased a property with someone else, in which case the scheme will cover only 50% of your loan.

Conclusion

No best options or best insurance only the most suitable. There’s still some technical issue or clause involve but no worry just remember to disclose your condition, and the above will be sufficient to help you unless you have special conditions like cancer, heart attack, mental issue & etc then it is advisable that you should speak to an insurance agent.

There’s still some cases / issues not discussed here because I’m worried that the article might be too long will put you into sleep. I will try to put them into another article.

Let me know what you think about my article by commenting or just WhatsApp me 😀 if you spot any mistake or error or anything else I didn’t cover. See you in the next article or video.

If you like my style / article, I have other articles for you:

Here’s the references for the research I’ve done after read through more than 10 articles if you’d like to take a look

- The Complete Guide To MRTA, MLTA, MRTT, And MLTT In Malaysia

- MRTA and MLTA: Don’t Let Your Need to Protect Your Home Be Used Against You

- 6 Popular Myths About MRTA And MLTA That Aren’t True At All

- MRTA vs MLTA: Which mortgage insurance is better?

- Know Your Stuff: Do you need home loan insurance?

MLTA Allianz: Link

MLTA Cimb: Link

MLTA Great Eastern: Link

Hong Leong Assurance: Link

AIA MLTA MRTA Insurance: Link

MLTA or MRTA Public Bank: Link

MLTA AIA: Link

MLTA Prudential / MRTA Prudential: Link

Manulife Life insurance: Link

MLTA RHB / RHB Insurance: Link

MRTA Ambank: Link

MRTA Affin: Link